Who Will Have Health Insurance in the Year 2025?

One Pagers | Nov 15, 2005

Jennifer DeVoe, MD, DPhil; Marty Dodoo, PhD; Robert Phillips, MD, MSPH; Larry Green, MD

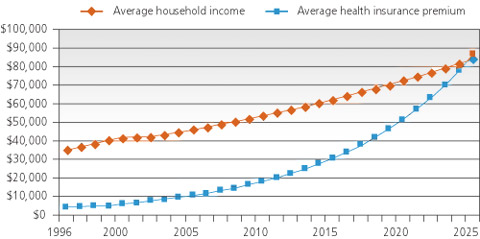

If current trends continue, U.S. health insurance costs will consume the average household's annual income by 2025. As health care becomes unaffordable for most people in the United States, it will be necessary to implement innovative models to move the system in a more equitable and sustainable direction.

In 2004, premiums for employer-sponsored health insurance increased by 11.2 percent—the fourth consecutive year of double-digit increases—outpacing the 2004 national wage increase of 2.2 percent.1 Employers increasingly view health insurance as an unaffordable benefit. Already, only one half of employers with fewer than 10 employees offer health insurance. Larger employers are outsourcing jobs and shifting more of the health care costs onto their employees who, in some cases, cannot afford to purchase coverage for their families.2 If health insurance premiums and national wages continue to grow at current rates, the average cost of a family health insurance premium will surpass the average annual household income by 2025 (see accompanying figure),2,3 approximately the time when the Medicare trust fund is projected to be insolvent.4

Figure. Annual family health insurance premiums compared with household income, 1996 to 2025

NOTE: Projections for 2003 to 2025 were extrapolations of the 1996 to 2002 average annual increase rates (3.03 percent for incomes and 10.83 percent for insurance premiums) using 2002 data as baseline. Information from references 2 and 3.

NOTE: Projections for 2003 to 2025 were extrapolations of the 1996 to 2002 average annual increase rates (3.03 percent for incomes and 10.83 percent for insurance premiums) using 2002 data as baseline. Information from references 2 and 3.

With health insurance packages bought and sold as profitable commodities, adequate health insurance coverage will soon be a product of shrinking benefits, to be bought by the wealthy and sold to the healthy. Most individuals cannot shoulder the burden of rising health care costs, and medical expense now tops the list of reasons for personal bankruptcy.5,6 If the system remains the same, the number of uninsured will continue to grow.

Shifting health care coverage from a commodity to a social good could reduce disparities and produce better population health. Changes in health care coverage will require more equitable and sustainable models of health care delivery and aligned advocacy to support them. The instability of health care financing and delivery provides an opportunity for family physician leaders to develop new models of efficient practice, with care that is accessible to everyone.7

References

- Kaiser Family Foundation and The Health Research and Educational Trust. Employer health benefits 2004: annual survey. Menlo Park, Calif.

- Medical Expenditure Panel Survey. Index of insurance component tables (health insurance cost study) 1996-2003.

- U.S. Census Bureau. Table H-8. Median household income by state: 1984 to 2003.

2005 Annual report of the Boards of Trustees of the Federal Hospital Insurance and Federal Supplementary - Medical Insurance Trust Funds. Washington, D.C., March 23, 2005.

- May JH, Cunningham PJ. Tough trade-offs. Issue brief no. 85. Washington, D.C.: Center for Studying Health System Change, June 2004:1-4.

- Jacoby MB, et al. Rethinking the debates over health care financing. New York University Law Review 2001;76:375-418.

- Martin JC, et al. The future of family medicine. Ann Fam Med 2004;2(suppl 1):S3-32.

The information and opinions contained in research from the Graham Center do not necessarily reflect the views or the policy of the AAFP.

Published in American Family Physician, Nov 15, 2005. Am Fam Physician. 2005;72(10):1989. This series is coordinated by Sumi Sexton, MD, AFP Associate Medical Editor.